Contents

Bankroll Management Sports Betting: 2026 Survival Guide

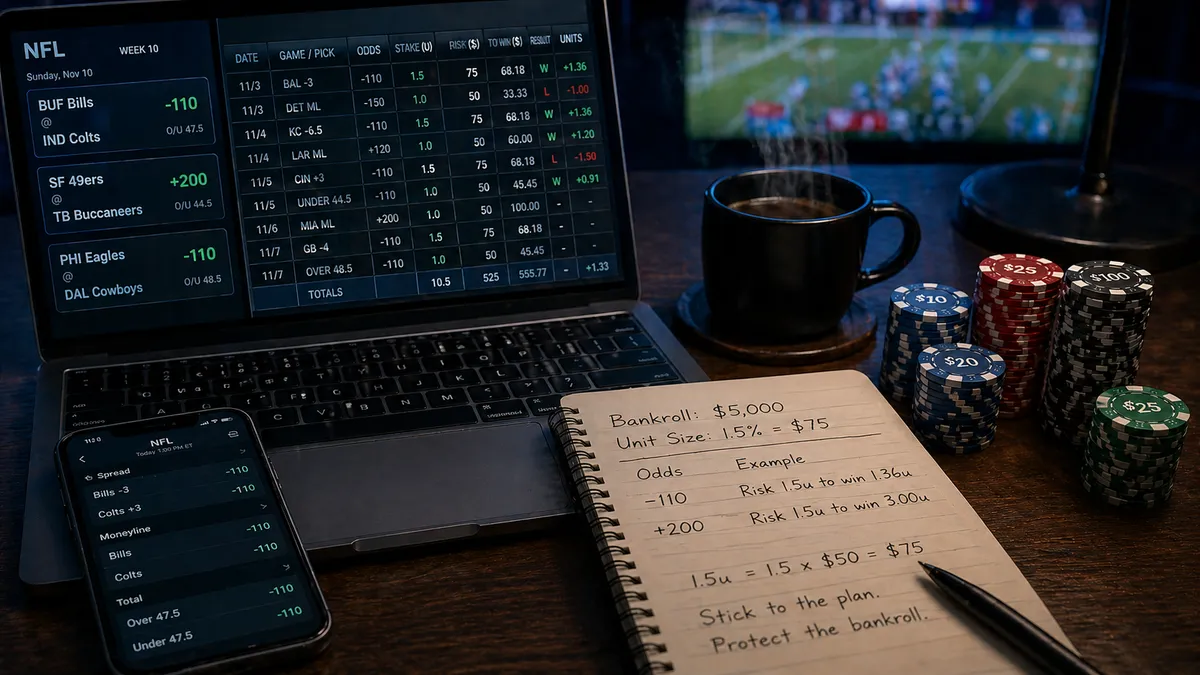

Picture this: It is Week 8 of the NFL season. You started with a $3,000 bankroll, hit a +$1,200 stretch in September, and decided "the model is working", so you bumped your unit from $50 to $90. Three weeks later, two bad Sundays later, your bankroll is at $1,400 and shrinking. You did not lose your edge. You lost the bankroll math.

Less than 5% of established sports-betting accounts are believed to be profitable, and the gap between the survivors and everyone else is rarely about picks. It is about how much you bet, when you bet it, and whether your stack is sized for the variance you are actually taking on. A bettor with a +2% edge and a 50-unit bankroll has a 36% risk of ruin. The same bettor with a 200-unit bankroll has a ~3% risk of ruin. Same edge. Different math. Different outcome.

This 2026 guide walks through the only sports-bankroll framework that actually holds up: four bettor archetypes mapped to real unit sizes, sport-by-sport variance numbers, the parlay-vs-singles bankroll multiplier most guides hide, and CLV math that tells you whether your edge is real before your win rate does. Two interactive tools, an archetype chart and a full sports-betting bankroll calculator, let you plug in your own numbers. By the end you will know exactly how big your bankroll needs to be to survive the season you are actually playing.

TL;DR, Quick Bankroll Reference

Key Numbers You Need to Know

| Bettor Archetype | Unit Size | Bankroll for $75 Unit | Annual EV at +2% Edge (1,000 bets) |

|---|---|---|---|

| Casual recreational | 2-3% | $2,500 - $3,750 | +$1,500 |

| Disciplined hobbyist | 1-2% | $3,750 - $7,500 | +$1,500 |

| Semi-pro grinder | 0.5-1% | $7,500 - $15,000 | +$1,500 |

| Professional sharp | 0.25-1% (variable) | $15,000+ | +$1,500 - $3,000 |

💡 For how sports bankroll fits with poker, blackjack, and casino sizing, see the pillar bankroll management guide.

The pattern: as you climb the discipline ladder, you bet a smaller percentage of a bigger bankroll. The annual EV stays the same at the same edge, but ruin probability collapses from 25%+ for the casual to under 1% for the pro. Bankroll size buys you survival, not extra profit. The full math is in our betting bankroll calculator.

Why Sports Betting Has a Bankroll Problem

Sports betting looks deceptively close to a 50/50 coin flip, most spread and total markets settle near 50%, and that surface impression hides why bankrolls implode so fast. The math underneath is built around the -110 vig, which means break-even win rate is 52.4%, not 50%. Bettors who win 51% of their picks lose money. Bettors who win 53% are profitable. The gap between losing and winning is two percentage points of accuracy, and most amateur bettors live inside that gap without realizing it.

The 52.4% Break-Even Wall

At standard -110 odds you risk $110 to win $100. Across 1,000 bets at exactly 50% win rate you lose $5,000 to the vig. To break even you need to win 52.38%, roughly 524 of 1,000. Hitting 53% gives you a $400 profit. Hitting 55% (the realistic ceiling for most disciplined bettors) gives $4,500. The space between disaster and modest profit is small enough that bankroll management becomes the dominant variable.

Why Variance Eats Bankrolls Faster Than Edge Recovers Them

Even a +2% edge bettor takes losing streaks of 8-10 in a row across a typical season. At -110 the probability of 8 straight losses for a 53% bettor is about 2.4%, meaning across 200 betting weeks (roughly 4 NFL seasons) you will hit at least one streak of 8 losses with high probability. If your unit is 5% of bankroll, that streak vaporizes 40% of your stack before any recovery. If your unit is 1%, the same streak burns 8%. Same streak, same edge, vastly different survival.

The Real Edge Most Bettors Have (Hint: It's Not Picks)

Pros consistently report that picks are the smaller half of their edge. The bigger half is line shopping (2-3% extra ROI), bonus farming early in a sportsbook account (5-15% one-time boost), and CLV discipline (only firing bets that beat closing line by 2c+). A bettor with a flat 50/50 record but +3% CLV across 1,000 bets ends the year roughly +$2,500 from a $5,000 starting bankroll. None of that profit comes from picking winners, it comes from systematic bankroll discipline applied to better-priced bets.

The Four Sports Bettor Archetypes

The same $5,000 bankroll means dramatically different unit sizes and ruin probabilities depending on which archetype you fit. Get the archetype wrong and your unit is wrong. Self-honest classification matters more than aspirational classification, most bettors who think they're "disciplined hobbyists" actually behave like "casual recreational" players in practice.

Casual Recreational Bettor (1-3% Units, No Edge Tracking)

The casual sits at $50-$150 units on a $3,000 bankroll, fires picks based on team affiliation or gut, and rarely tracks results beyond the running balance on the app. Effective edge against the book is -2% to -4% (vig plus mistakes). Variance per bet is high because parlays and SGPs are over-represented in the slate. Required bankroll to last a full NFL season at typical betting volume: 100-200 units. Real ruin probability over a 4-month season at 3% unit size: 35-50%. The casual is not a profitable archetype, bankroll management for them is about extending the entertainment, not generating profit.

Disciplined Hobbyist (1-2% Units, CLV Tracking, Occasional Fractional Kelly)

The hobbyist tracks every bet in a spreadsheet, beats closing line by 1-2c on average, and uses 1-2% flat units with the discipline to not chase. Edge is roughly 0% to +2% net of vig, close to break-even. Variance is contained by avoiding parlays except for genuine value SGPs. Required bankroll: 100-200 units. Ruin probability at +1% edge with 150 units: ~10%. The hobbyist is the largest archetype of "winning" bettors, though their hourly profit is modest.

Semi-Pro Grinder (0.5-1% Units, Full Tracking, Line Shopping)

The grinder uses 3-5 sportsbook accounts, beats closing line by 3-5c on average, and runs 0.5-1% units with fractional Kelly adjustments based on quantified edge. Edge is +2% to +4% net of vig. Variance is actively managed by avoiding high-vig markets (futures, parlays >3 legs) and concentrating on -110 spreads, totals, and selectively priced moneylines. Required bankroll: 200-400 units. Ruin probability at +2% edge with 300 units: ~1%. The grinder is profitable in absolute dollars and earns real hourly returns once volume crosses 1,500 bets/year. Math behind their unit sizing aligns with our bankroll risk of ruin guide.

Professional Sharp (Confidence-Weighted Variable Units)

The pro varies bets from 0.25% to 1.5% of bankroll based on quantified edge per pick, runs 5-10 books with active limit management, and beats closing line by 5-8c on edge plays. Edge is +3% to +6% net of vig. Variance is managed through portfolio construction across sports and bet types, they are functionally running a hedge fund inside the sports markets. Required bankroll: 500+ units. Ruin probability at +4% edge with 500 units: <0.1%. Pros graduate beyond bankroll-as-survival into bankroll-as-capital, where the question shifts from "how do I avoid ruin" to "what is my optimal Sharpe ratio."

| Bettor Archetype | Recommended Bankroll | Unit Size | Annual EV (+2% edge) |

|---|---|---|---|

| Casual Recreational | 3000 | 75 | 1500 |

| Disciplined Hobbyist | 6000 | 75 | 1500 |

| Semi-Pro Grinder | 12000 | 75 | 1800 |

| Professional Sharp | 22500 | 75 | 3000 |

The chart above plots recommended bankroll, unit size, and annual EV at +2% edge across all four archetypes for a comparable $75 average unit. The bankroll requirement triples from casual to pro, but EV stays similar, discipline buys survival, not raw return.

One Practical Rule

If you are not actively tracking CLV after every bet, you are a casual recreational regardless of how you self-identify. Move down one archetype and use the more conservative unit size until your record (with CLV) earns the next tier.

Bankroll Math by Bet Type

Sports betting is not one game. It is a dozen games disguised as one app. Each bet type, spreads, totals, moneylines, parlays, SGPs, props, futures, live, has its own variance signature, and bankroll math has to bend around the type, not just the sport.

Spreads and Totals (-110 Standard, Lowest Variance)

Spreads and totals at -110 are the workhorse market: ~50/50 outcomes, single-bet variance equal to one unit's standard deviation. A flat-staking bettor at 1.5% units needs 100-150 units to survive the season at break-even win rate. Across 1,000 bets, ruin probability at 53% true win rate with 100 units: ~6%. With 200 units: <0.5%. Spreads are the easiest market to bankroll because variance is bounded, you cannot have a single bet that wipes out a week.

Moneylines (Variance Scales With Odds)

Moneyline variance depends on the odds. A -200 favorite (66.7% to win) has lower variance than a coin flip, wins are smaller but more frequent. A +200 underdog (33.3% to win) has higher variance, losses are more frequent and the recovery wins pay larger. Bettors playing only +150 to +300 underdogs need 1.5x the bankroll of pure spread bettors to maintain the same ruin probability, because longer odds spread the variance window across more bets before the wins land.

Parlays and SGPs (Variance Multiplier)

A 3-leg parlay at +600 has roughly 6x the variance of a single -110 bet. A 4-leg at +1,000 runs about 10x. A 5-leg at +2,500 hits 20x. To keep ruin probability constant when variance multiplies by 10, your bankroll needs to roughly quadruple. Concrete: a $5,000 bankroll handling 1,000 spread bets at 1.5% units fine produces 30%+ ruin probability if the same dollar volume runs through 4-leg parlays. This is why parlay-heavy bettors blow up faster than their pick win-rate would predict, and why the variance buffer in our universal bankroll calculator climbs sharply once you toggle parlay-heavy stakes.

Player Props and Live Betting (High Variance, Edge Opportunities)

Props at -150 to +150 cluster around moderate variance per bet but are typically over-bet by recreational bettors who chase narrative angles. The edge opportunity is real, bookmakers shade soft on lower-volume markets, but variance per bet is 1.5-2x straight spread variance because bookmaker error is high. Live betting variance is similar but with timing pressure that produces more emotional sizing errors. Bankroll math for prop-heavy bettors: 200+ units minimum, with strict 1% caps per pick regardless of perceived edge.

Futures Markets (Capital Lock-Up Problem)

Futures (Super Bowl winner, MVP, division titles) lock up bankroll for months. A $200 Super Bowl future placed in August does not return to your usable bankroll until February at earliest. The bankroll math has to treat futures as illiquid capital, typically capped at 5% of total bankroll across all open futures regardless of perceived edge. The long-tail variance and bookmaker hold (often 25-40% built into futures pools) make these the worst market for bankroll-constrained bettors.

Sport-by-Sport Variance Differences (2026 Data)

Variance is not just about bet type, it varies by sport too. Same 1.5% unit applied to NBA totals and NFL props produces dramatically different bankroll burn rates because the underlying outcome distributions are different.

NBA: Lowest Variance, Best for Bankroll Building

NBA spreads and totals are close to 50/50 with high game volume (1,230 regular season games + playoffs). Single-bet variance is among the lowest in major sports. A 1.5% unit bettor at break-even win rate sees roughly $300-$400 swings per 100 bets on a $5,000 bankroll, manageable drawdowns. NBA is also the highest-volume sport for sharp action, meaning closing lines are tight and CLV is harder to capture but easier to verify.

NFL: Medium Variance, Highest Stakes per Bet

NFL has only 272 regular-season games, meaning bettors over-concentrate stakes per game. Variance per bet is higher than NBA because the limited game volume drives larger bet sizes for the same weekly action. NFL spread variance is similar to NBA, but NFL totals carry slightly higher variance because key numbers (3, 7, 10) cluster scoring outcomes. Bankroll requirement for full-season NFL play at 1.5% units: 150-200 units minimum.

MLB: High Variance, Long Season, Underdog Plays

MLB has 2,430 regular-season games, highest volume of any major sport, but variance per bet is high because moneylines dominate and odds spread from -250 to +200 routinely. Underdog plays carry +120 to +200 variance, and small home-dog edges are the most-cited profitable angle. Bankroll requirements: 200+ units for MLB-only bettors at 1% units. The long season produces real sample-size data faster than other sports, by mid-July you have 1,500+ games of evidence.

NHL: Highest Variance Major Sport, Hardest on Bankrolls

NHL combines low-scoring game outcomes with frequent overtime and shootout decisions, producing the highest single-bet variance of major sports. A puck-line spread (-1.5 / +1.5) shifts dramatically based on a single bounce or empty-net goal. NHL bettors need 250+ units of bankroll for the same ruin probability that NBA bettors hit at 150 units. Most disciplined NHL bettors avoid single-game props entirely and stick to 60-minute moneylines with reduced unit sizes.

Soccer: Variable by Market, Long Tail in Outright Markets

Soccer 1X2 markets on major leagues run reasonable variance but outright winner markets (Premier League champion, Champions League winner) hit extreme variance with 12-25% bookmaker hold built in. Asian handicap markets normalize variance close to NBA spread levels. Soccer bankroll math depends entirely on which market mix you play.

The Compounding Trap and Other Bankroll Killers

The math problems are solvable. The behavioral problems are what actually kill bankrolls. Four patterns destroy more sports-betting accounts than bad picks ever did.

Increasing Units After a Winning Streak

A 6-game winning stretch is variance, not skill, at 53% true win rate the probability of 6 straight wins is 2.5%, which means you'll experience this streak roughly once every 40 days of betting. Bettors who bump units from 1.5% to 3% after a winning week then face the next inevitable cold streak with double the bet size. The math: a 2x unit increase makes a typical 8-loss cold streak 4x more damaging in dollar terms. Stay flat. Re-size on a calendar schedule (monthly), never on a streak.

Chasing Losses

Chasing, increasing bets after a loss to "win it back", is the textbook bankroll killer. The math is brutal: doubling unit size after each loss requires winning 50%+ from then on to recover, but the initial losing run already weighted your bet sequence toward the largest stakes at the worst moments. Most chasing patterns exit at -50% bankroll within 3-5 bets. The rule: never modify unit size based on the previous bet's outcome. Re-size only on a fixed schedule.

No Stop-Loss Trigger

Sitting down each weekend with no defined exit point. Bettors without a written stop-loss continue firing through 50%+ drawdowns because each individual bet feels small. Recommended trigger: 30% drawdown from peak bankroll prompts a 7-day cooling period and a 200-bet audit of recent picks. 40% triggers a unit-size cut to 50% until lost ground recovers. These rules sound conservative but prevent the death spiral.

Mixed Bankrolls

Using sports betting bankroll for casino plays, day trading, fantasy contests, or any other activity where ruin math differs. Each non-sports bet shrinks the playable balance below your unit-sizing math without you noticing. By month three the bankroll is a fiction. Solution: a dedicated sportsbook bankroll separate from any other gambling activity, tracked in a master spreadsheet with deposit/withdrawal stamps. Compare with the discipline required for our bankroll management blackjack framework, casino bankroll math has similar foundations but variance differs.

CLV: The Only Profit Predictor That Beats Win Rate

Closing line value is the difference between the odds you bet and the odds at game start. If you bet a -3 spread at -110 and the line moves to -4 at kickoff, you got "+1 point of CLV." Across hundreds of bets, average CLV is the single best predictor of long-term profitability, better than win rate, ROI, or any other metric.

Why CLV Predicts Better Than Win Rate

The closing line is the sharpest market state, it incorporates all the late-arriving information from injuries, weather, and sharp action. If you consistently beat it, the market itself is telling you your bets had value before the line moved. A bettor with 49% win rate but +3c CLV is sharper than a bettor with 53% win rate at -1c CLV. The +3c CLV bettor is just unlucky in their first 200 bets; the 53% / -1c CLV bettor is profiting from variance that will revert.

Tracking CLV: The Spreadsheet Practice

Every bet logged with: date, bookmaker, line you got, line at kickoff, result. Compute CLV as the difference in implied probability between your odds and closing odds. Average across 100+ bets to see if you're consistently ahead. Tools that auto-track this exist (Pikkit, Outlier, Unabated), but a basic spreadsheet works.

What CLV Tells You About Bankroll Sizing

Positive CLV across 200+ bets justifies fractional Kelly sizing, you have proven edge. Negative CLV at any sample size says drop unit size or stop betting that market entirely. Neutral CLV (within ±0.5c) says you're break-even-to-slightly-positive, flat 1% units are appropriate, fractional Kelly is premature.

CLV and Bookmaker Limits

Sportsbooks track CLV on their end and flag bettors who consistently beat closing lines. Hitting +3c CLV across 500+ bets gets you limit-restricted at most major books. The mature bankroll strategy splits action across 3-5 books and accepts that limits are part of the game.

What Positive CLV Says About Unit Sizing

Once you have 200+ bets logged with positive CLV, the math earns you a small unit-size raise, typically from flat 1% to fractional Kelly sized at quarter-Kelly. Run the numbers in our Kelly criterion calculator before changing anything: full Kelly is dangerous because edge estimates are imprecise; quarter-Kelly captures most of the growth without the drawdown spikes that wreck real-world stacks.

Worked Examples and Calculator

Two concrete scenarios that come up in nearly every sports bankroll question. Plug your own numbers into the calculator below to see how the math shifts.

The calculator above lets you flex archetype, bankroll size, edge percentage, betting volume, average odds, and sport variance to see expected EV, drawdown estimate, ruin probability, and the time-to-double figure for positive-edge bettors.

Example 1, $5,000 Bankroll, 1.5% Units, +2% Edge, 1,000 Bets/Year

Inputs: $5,000 bankroll, $75 unit (1.5%), break-even at -110, true 53.5% win rate (+2% edge), 1,000 bets across NFL/NBA/MLB.

Math: Expected EV = 1,000 × $75 × 0.02 = +$1,500 annual. Standard deviation per bet ≈ $75. Across 1,000 bets, total SD ≈ $75 × √1,000 ≈ $2,370. Maximum drawdown estimate ≈ 1.5 × SD = $3,555. Ruin probability across the season: ~3-4%.

Verdict: $5,000 at 1.5% units survives a typical season comfortably with $1,500 expected profit, but the drawdown estimate ($3,555) shows you'll likely see your bankroll dip below $1,500 at some point during the year. Mental preparation for that drawdown is part of the bankroll plan. Plug the same numbers into our free bankroll tool to see how the curve shifts when you change unit size from 1.5% to 1%, drawdown shrinks by 33%, but EV is unchanged.

A Note on the 1,500-Bet Threshold

If your annual betting volume is below ~500 bets, sample-size noise dominates and the math in this example is partly aspirational. Below 500 bets a "win rate" estimate has 8-10 percentage points of confidence interval, meaning your "53.5% bettor" might actually be a 49% bettor having a hot run, or a 58% bettor having an unlucky draw. Bankroll math gets reliable around 1,000 bets and rock-solid past 2,000.

Example 2, $2,000 Bankroll, 3% Units, Casual at -1% Edge, 500 Bets/Year

Inputs: $2,000 bankroll, $60 unit (3%), 51.4% win rate (-1% edge after vig), 500 bets including parlays.

Math: Expected EV = 500 × $60 × (-0.01) = -$300 annual. SD per bet ≈ $60 (singles) but ~$120 with 30% parlay volume. Total SD ≈ $120 × √500 ≈ $2,680, larger than the bankroll. Ruin probability across the season: 35-45%.

Verdict: $2,000 at 3% units with negative edge and parlay variance is structurally a coin flip on whether you finish the season with money. The math says: drop to 1.5% units ($30 each), eliminate parlays, and the ruin probability falls below 15% for the same expected loss. Or accept that this is entertainment, size for entertainment ($30/week budget), and stop calling it bankroll management.

Multi-Sportsbook Bankroll Strategy

Single-book bankroll is a rookie mistake for any bettor with $1,000+ to deploy. The math for splitting across 3-5 books captures real edge that no single book offers.

Why Multi-Book Splits Work

Three structural edges: line shopping (the same -3 spread might be at -110 at one book and -105 at another, worth ~2% ROI annually), bonus farming (signup matches at $500-$5,000 per book multiply effective bankroll), and limit avoidance (sharp action gets limited at any single book within months). A bettor running $5,000 across DraftKings, FanDuel, BetMGM, and Caesars effectively has a different bankroll than one with $5,000 at a single book.

Recommended Split: 30/25/25/20

40% on the primary book where you have the most account history and best limits, 25% on a secondary, 25% on tertiary, 10% reserve in non-betting account for monthly rebalances. Each book's "balance" is visible to you separately, but unit sizing comes from the total bankroll, not per-book. Never let any single book hold more than 40% of total, concentration risk is real if a book limits, freezes, or processes a withdrawal slowly.

Avoid Cross-Book Hedging Mistakes

A common error: placing both sides of the same game at different books to "lock in profit" from a small line difference. The math rarely justifies it after vig, only true arbitrage opportunities (spreads of 4%+ across books) are worth executing, and those are rare and quickly closed.

Never chase without doing the math. Our dogon (martingale) calculator shows the bankroll a recovery chase demands.

Off the sportsbook and onto the course? See golf betting games for on-course formats and side bets with friends.

Frequently Asked Questions

Evgeniy Volkov

Verified ExpertFullstack developer with a background in mathematics. I build the calculators and game-style tools on ToolsGambling with Pixi.js and modern web tech, and every result uses transparent probability formulas you can verify yourself.